Equities Market Research

Trending

Market Metrics That Matter: Your Monthly U.S. Cash Equities Volume Briefing

Cboe BYX® Equities Exchange (BYX) Periodic Auctions had over 1,562 unique stocks entered this month. Learn more about Periodic Auctions here. September notional traded value was $81.1 million with 1,231 distinct stocks trading.

Read MoreSeptember Highlights

- Chris Isaacson, Executive Vice President, Chief Operating Officer, participated in the SEC Regulation NMS roundtable advocating for retaining Rule 611 but with targeted modifications. Cboe believes that Rule 611 of Regulation NMS is worthy of review. As always, though, Cboe notes that changes to any one rule can have cascading impacts on other requirements and on the incentives that ultimately shape the marketplace. In this regard, it is important that we consider these implications when considering any significant change to Rule 611. Read Cboe’s letter to the SEC here.

- Cboe BYX® Equities Exchange (BYX) Periodic Auctions had over 1,562 unique stocks entered this month. Learn more about Periodic Auctions here.

- September notional traded value was $81.1 million with 1,231 distinct stocks trading.

- Cboe announced support for transaction fees for U.S. equities as part of the ongoing process of adapting to new SEC rules. Learn more.

Upcoming Changes

November 7, 2025 | Cboe BZX® Equities Exchange (BZX) will update Limit-On-Close (LOC) and Late-Limit-on-Close (LLOC) order behavior to improve Closing Auction stability and enhance price discovery.

News and Insights

- How Cboe is Supporting the Growing ETF Market

- Cboe Plans to Launch Cash-Settled Futures and Options on New Index Tracking Tech and Growth-Orientated U.S. Stocks

- Cboe Plans to Launch Continuous Futures for Bitcoin and Ether, Beginning November 10

U.S. Listings

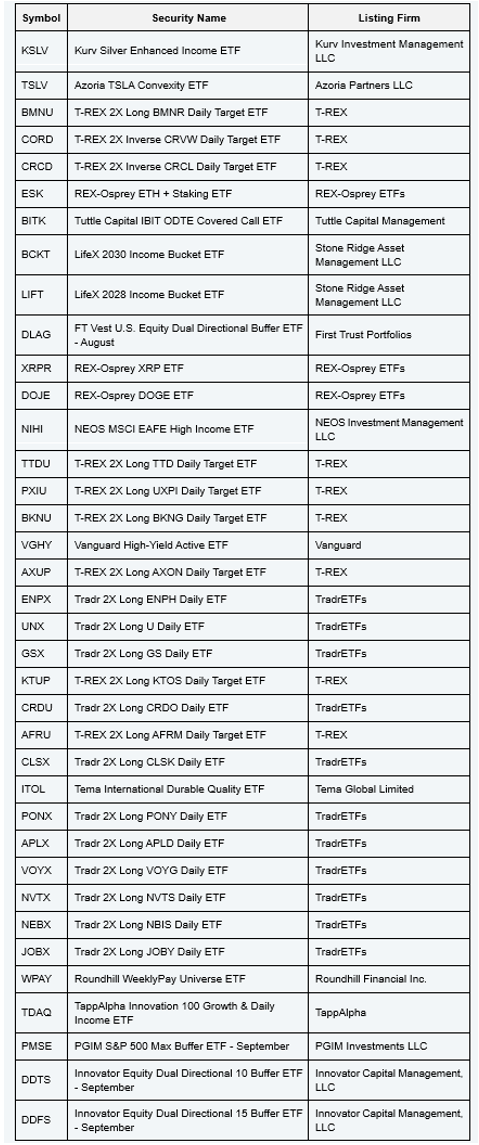

In September, 37 new Exchange Traded Funds (ETFs) were listed on BZX.

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More

-

Read More