Read More

Recently, Alphabet (GOOGL) and Amazon (AMZN) — two of the largest companies by market capitalization —both announced 20:1 stock splits. More recently, GameStop Corp (GME), potentially the most famous of the 2021 retail “meme” stock phenomenon ,” announced a 10:3 split. Investors responded positively, as the price of the underlying securities rallied in the trading sessions immediately following the announcement. With stock splits making headlines, Cboe’s North American Execution Consulting Team analyzed potential changes to underlying securities, pre- and post-split, from a market structure perspective in both equities and options markets.

The team used unique data sets from Cboe Data Shop to examine the market structure behavior of all stocks that performed a forward split since 2020. Out of 61 stocks across all market capitalization categories, three mega-cap stocks (companies with market capitalization above $200 billion dollars) have split since 2020: Apple (AAPL), Tesla (TSLA) and Nvidia (NVDA). The team chose to analyze all stock splits by market cap in aggregate, as well as Apple’s 4:1 split individually, as a representative of mega-cap stocks. For each category, the team studied how stock splits impact securities over time, then how the splits impact various factors that impact a security’s value, including volume, notional exposure and volatility.

First, the team analyzed how stocks trade differently, if at all, in the immediate week after the split became effective and up to six months following for both equites and options. The week before the effective date of the split was used as the “pre-split” period. We measured changes in market structure behavior for these securities via a basket of metrics: volume, retail volume, notional exposure, trade size, odd-lot volume and volatility.

The team found that, on average, splitting a security does not necessarily increase liquidity or attract investors’ interest proportionally to the ratio at which the security was split. In some cases, the research shows such stock splits have an adverse effect on the notional value traded on the securities. However, the evidence suggests that stock-split events drive additional participation from retail investors, especially in securities with larger market capitalization.

We then analyzed trading volume, particularly executed shares in equities and executed contracts in options, to understand the impacts of a split on the market structure behavior of the underlying security. Exhibits 1 and 2 below show the median percentage change in equities executed shares and options contracts traded before and after the effective date of the split. Volume in mega-cap equities initially spiked 342% the week immediately after the split (Exhibit 1). This initial growth declined during the six months following the split. From an options market structure perspective, mega-cap securities traded modestly in higher volume initially following the split and peaked at six months post-split (Exhibit 2). Large cap stocks also traded moderately higher initially, but, again, the effect declined with time. Volume was only marginally higher following the split in mid- and small-cap securities. In some small-cap securities, volume decreased sharply. These changes indicate that investors’ have a lukewarm appetite taking on risks in the options markets for mid- and small-cap securities following a stock split.

However, is there indeed a notable change in how a security is traded after a split as the raw, unadjusted data suggested? In theory, a stock split makes the security more affordable for investors with limited capital to deploy. Consequently, the affordability would attract more interests to trade the security post-split. To understand these changes better, we introduced “split-adjusted” calculations to our metrics, which normalizes the metrics by the split ratio. For example, 400 Apple shares traded post-4:1 split would equate to 100 split-adjusted shares traded.

After applying this calculation, that the data shows that median volume traded did not see a substantial increase following the split. In equities, split-adjusted volume in mega-cap securities increased slightly one-week post-split. However, in the two-week to six-month period post-split, the median executed shares volume decreased about 48%,compared to volume a week pre-split (Exhibit 3).

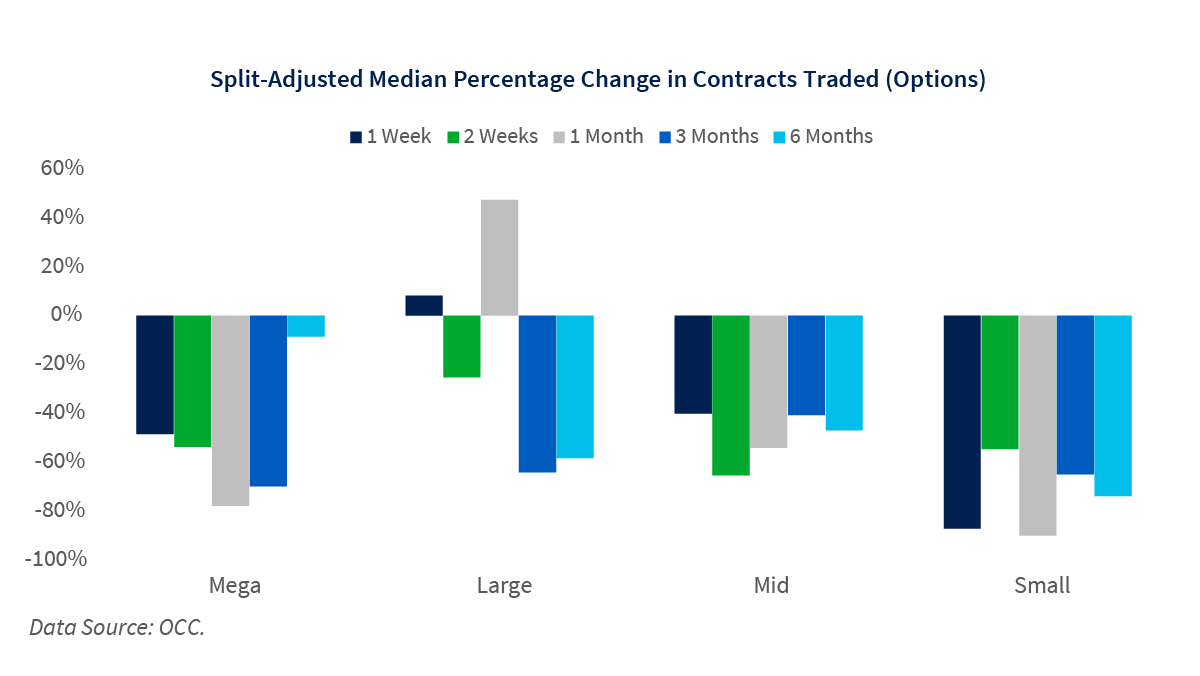

The options market followed a similar trend, with a decrease in the number of split-adjusted options contracts traded in the weeks and months following the split across all market cap groups. The median number of contracts traded in mega-cap stocks decreased approximately 49% one week post-split (Exhibit 4). This evidence contradicts the affordability theory above Preliminary evidence suggests that post-split lower prices do not necessarily attract significant additional interest in trading the securities.

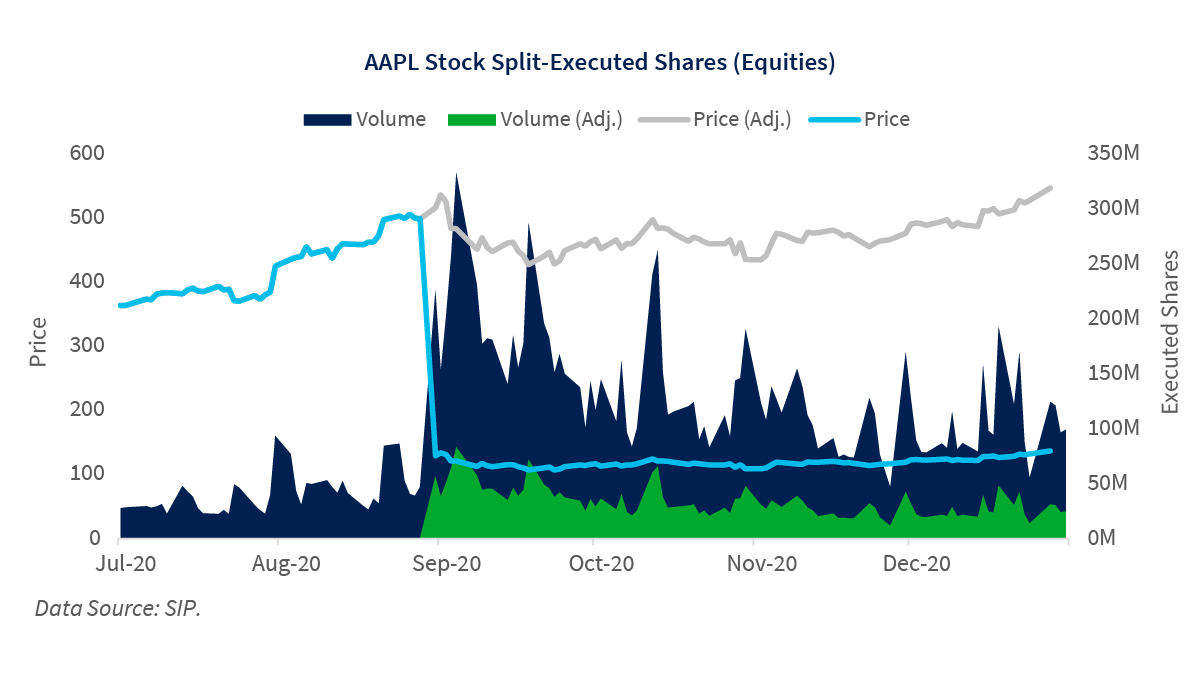

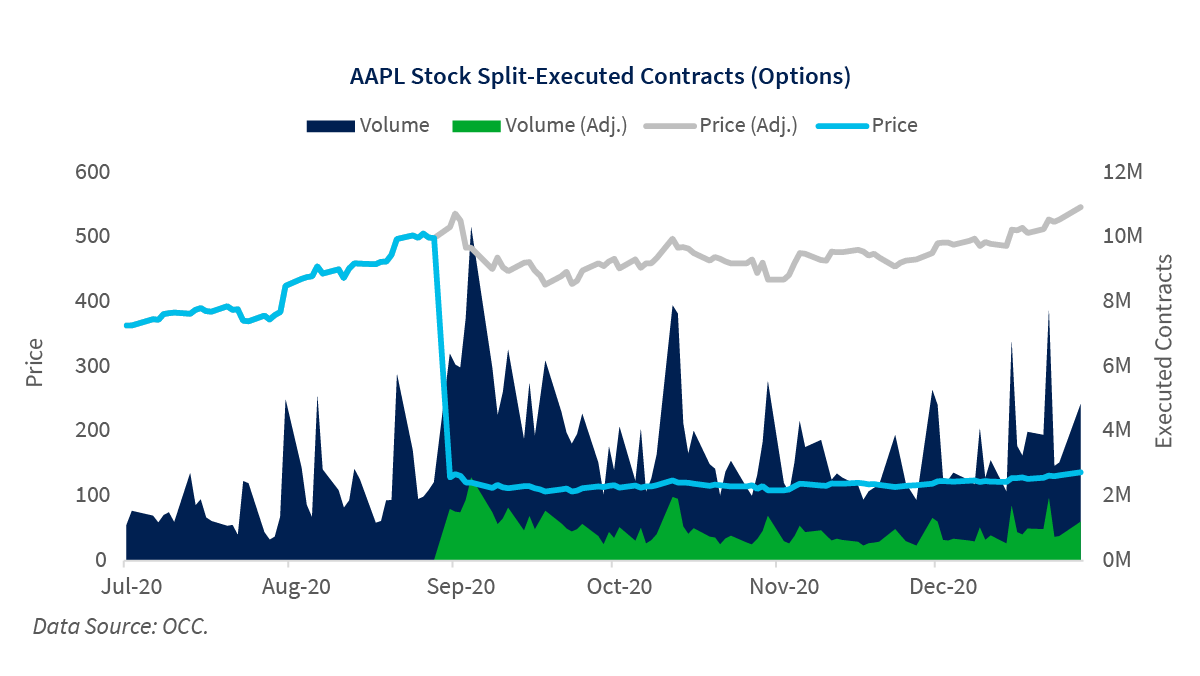

To put these findings in clearer focus, we reviewed Apple’s 2020 forward split as a case study. Apple announced a 4:1 stock split on July 30, 2020, which became effective on August 31, 2020. On August 31, Apple’s share price went from $502 per share to $129 per share. Executed shares volume increased 382%. from 47 million shares the day before the split to 225 million shares on August 31.However, after applying split-adjusted calculations, we see that executed shares volume remained flat (Exhibit 5). Likewise, in the options markets, there was a 52% decrease in the split-adjusted number of contracts traded, averaging 0.9 million contracts traded daily post-split compared to 1.9 million contracts traded daily pre-split (Exhibit 6).

Retail market structure was an integral part of this analysis, as retail investors on average tend to trade in smaller sizes due to their limited capital, relative to institutional investors. Theoretically, if the theory that stock splits would attract more investors due to lower security price holds true, we should expect higher split-adjusted retail volume post-split. However, empirical evidence shows that, with the exception of mega-cap securities, in which initial Cboe retail-attested executed share volume increased, securities from other cap groups traded with less retail volume on an adjusted basis post-split. This effect is more pronounced in options markets. Split-adjusted OCC-defined customer volume — a proxy for retail trading volume — mostly decreased across all periods post-split (Exhibit 8). The changes in both the equities and options markets signal that retail and retail-proxy trading volume do not change in proportion to the ratio that the securities were split.

The trading behavior of Apple stock following its 2020 split aligned with the behavior observed in the overall equities and options markets. In options markets, Apple’s unadjusted post-split customer volume increased by 92%, averaging 1.7 million daily contracts executed, compared to 0.9 million contracts pre-split (Exhibit 10). Applying split-adjusted calculations shows that adjusted customer volume post-split only averages 0.4 million daily contracts executed, a 52% decrease compared to pre-split volume.

Notional value traded is a traditional benchmark to help understand whether stock splits renew interest from new investors who could not previously invest in certain stocks due to higher security prices. Our team posits that if the stock splits brought in new investors and existing investors are indifferent, on average, investors’ overall notional value traded to the security should increase. Empirical evidence, however, showed that notional value traded mostly decreased after stock-splits. In equities markets, mega-cap securities experienced an initial boost one week after the stock split went into effect, but declined significantly in the weeks and months following, decreasing up to 40% at three and six months later (Exhibit 11). Large-cap securities experienced marginal boosts in investor interest, from a notional perspective, but also declined following the initial boost (Exhibit 12). Mid- and small-cap securities never gained traction, and instead saw declines in investors’ net exposure immediately post-split and in the months thereafter. In the options markets, the decline in investors’ notional exposure is more pronounced. In mega-cap securities, investors’ net exposure increased initially but declined up to 60% in the following months, compared to pre-split levels.

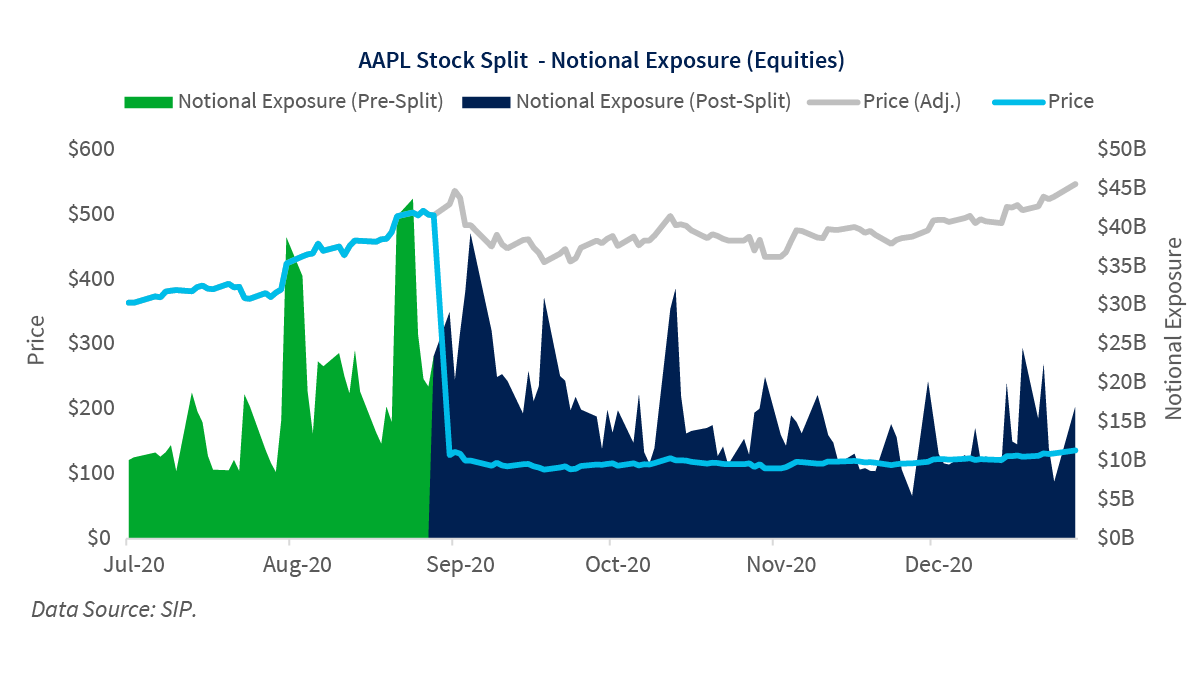

The Apple case study validates our empirical findings above as we see net notional value traded in the security declined immediately post-split and more sharply in the weeks and months following, averaging $15 billion daily, a 9% decrease compared to pre-spit levels (Exhibit 11). This effect is more pronounced in options markets. Investors’ average daily net notional value traded in Apple declined 47% post-split to $45 billion, compared to pre-split notional value traded (Exhibit 12). While splitting a security makes it more affordable, the evidence shows that it may unintentionally decrease additional investor interest.

For a more in-depth picture of how stock-splits impact market structure, we analyzed “trade size” and “notional trade size” metrics, which measure the number of shares or contracts traded and the gross dollar amount of exposure that investors take on with each trade, respectively. Exhibit 15 and 17 illustrate that investors executed a higher number of shares per trade post-split in equities markets but the notional exposure of those trades declined. This aligns with our observation that stock splits provide additional liquidity to markets as more shares and contracts change hands, but they do not necessarily inject a proportional amount of additional investments to the ratio that the security is split.

The results of the same analysis in the options markets were mixed. More contracts changed hands each trade post-split in mega-, large- and mid-cap securities, but the response was different in small cap securities (Exhibit 16). From a notional exposure perspective, investors risked less per trade in mega-, large- and small-cap securities post-split. There was a more immediate appetite for risks in mid-cap securities as the amount of notional per trade increased substantially in the week following the split (Exhibit 18).

Likely due to growth of zero-commission trading and increased retail participants, odd lot trading now comprises over 55% of all equity trades. As an important segment of overall equities trading, we also examined the potential impact of stock splits on odd lots trading. Exhibit 19 below shows that there were a significantly higher number of odd lots trades pre-split (23% - 36%) compared to post-split (15% - 23%) across all market capitalization groups.

Finally, we studied how stock splits impact volatility in split securities. Volume-weighted-implied volatility in mega-cap securities climbed in the immediate weeks following the split but drastically tapered off in the months following, then climbed again six months later (Exhibit 21). Large-cap securities, however, were consistently more volatile post-split. Mid- and small-cap securities mostly traded in less volatile manners following the split. These results may signal that investors’ renewed interests are mostly focused on securities with larger market capitalization.

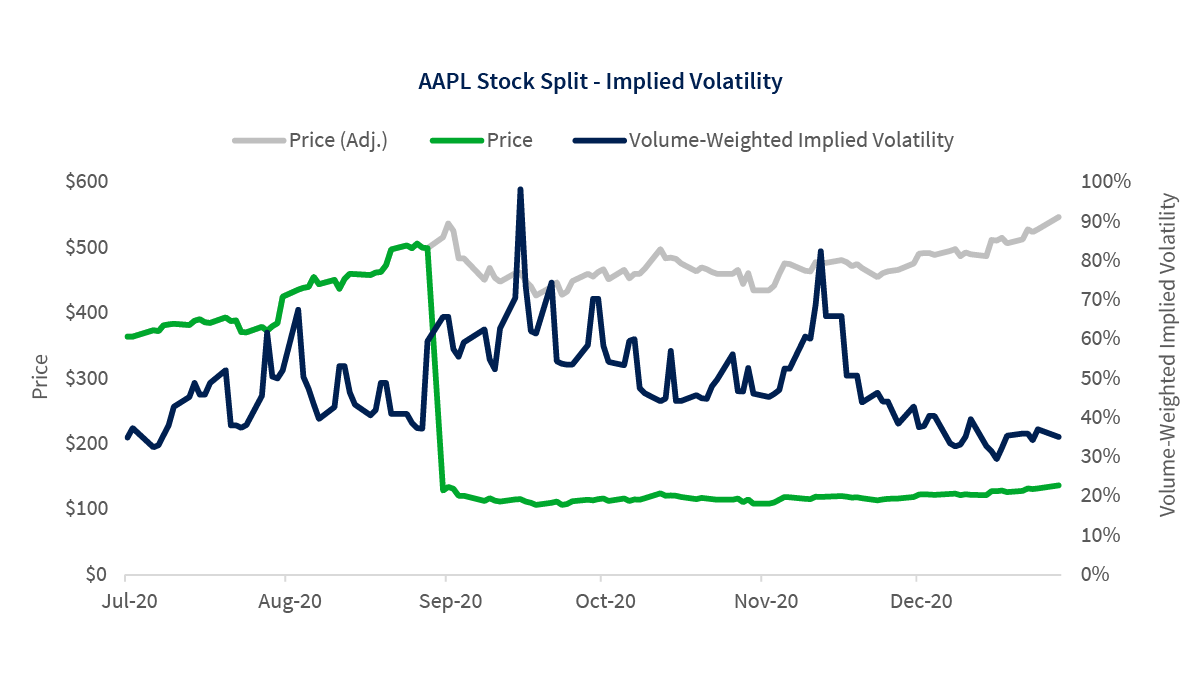

The changes in implied volatility in Apple following its split were consistent with the aggregate changes in mega-cap securities. Exhibit 22 shows an initial spike in volatility, but the effect mostly tapered off with time. As the initial excitement of the split event wears off, so does the security’s volatility.

On average, stock splits do not lead to increased liquidity that is proportional to the split ratio and appear to lead to a decrease in investors’ overall capital exposure to the split security. However, it is clear that stock-split events may drive additional participation from retail investors. As the retail trading community continues to grow, stock splits may interest companies seeking to make trading in their stock more accessible, however splits may be to the detriment of existing shareholders.

Cboe provides robust and resilient markets that bring together buyers and sellers across numerous asset classes. Recognizing the growth of retail trading and the importance it holds in today’s equities and options markets, Cboe’s North American Equities team is constantly innovating and developing solutions that address retail investors needs. Cboe’s trading mechanisms, such as Retail Priority, Quote Depletion Protection (QDP), Early Trading and Periodic Auctions improve liquidity and enhance our customers’ overall trading experience. Please reach out to our coverage team with questions and to learn how we can help you optimize your trading experience.

2022 Cboe Exchange, Inc. All rights reserved.

The information provided is for general education and information purposes only. No statement provided should be construed as a recommendation to buy or sell a security, future, financial instrument, investment fund, or other investment product (collectively, a “financial product”), or to provide investment advice.

Cboe®, Cboe Global Markets®, Bats®, BIDS Trading®, BYX®, BZX®, Cboe Options Institute®, Cboe Vest®, Cboe Volatility Index®, CFE®, EDGA®, EDGX®, Hybrid®, LiveVol®, Silexx® and VIX® are registered trademarks, and Cboe Futures ExchangeSM, C2SM, f(t)optionsSM, HanweckSM, and Trade AlertSM are service marks of Cboe Global Markets, Inc. and its subsidiaries.

Past performance of an index or financial product is not indicative of future results. Click Here to Unsubscribe. To unsubscribe by postal mail, please write to: Cboe Customer Experiences, 400 S. LaSalle St., Chicago, IL 60605 © 2021 Cboe Exchange, Inc. All Rights Reserved.