Regional Market Commentary

Trending

Strengthening Australia’s Public Markets into 2030 and Beyond: A Call for Further Competitive Reform

Australia’s public markets have long been regarded as the gold standard for transparent capital raising and efficient price discovery. Underpinned by a robust regulatory framework and supported by world-class financial infrastructure, these markets have served investors and issuers alike with integrity and resilience.

Read MoreAustralia’s public markets have long been regarded as the gold standard for transparent capital raising and efficient price discovery. Underpinned by a robust regulatory framework and supported by world-class financial infrastructure, these markets have served investors and issuers alike with integrity and resilience. Yet, as global capital flows become increasingly mobile and innovation accelerates across financial markets, Australia must evolve to remain competitive.

Cboe Australia has submitted a case to the Australian Securities and Investments Commission (ASIC) for regulatory reforms that would enhance competition, resilience and innovation in Australia’s public markets for the benefit of Australia’s investors and its community. These reforms are not only timely but essential to ensure that Australia continues to attract and retain global capital.

The Case for Reform

Cboe’s submission to ASIC’s discussion paper on the dynamics between public and private markets outlines four key recommendations.

1. Broaden the Clearing and Settlements (CS) Services Rules to include clearing and settlement services for exchange-traded equity derivatives.

2. Enhance governance of ASX’s clearing and settlement facilities to ensure greater transparency and stakeholder representation.

3. Review the vertical integration of the ASX Group, which currently dominates Australia’s financial market infrastructure.

4. Ensure market-neutral regulatory guidance, removing barriers that disproportionately affect new entrants.

Each of these recommendations is aimed at fostering a more competitive and resilient market environment – one that is better equipped to serve investors, support innovation and withstand operational shocks.

Why Public Markets Matter

Public markets are foundational to efficient capital formation. They offer transparency, liquidity and investor protection that private markets often cannot match. While private markets play a complementary role, particularly for early-stage companies, public markets remain the primary avenue for capital formation, broad investor participation and long-term wealth creation.

Cboe’s global experience highlights three critical features of strong public markets.

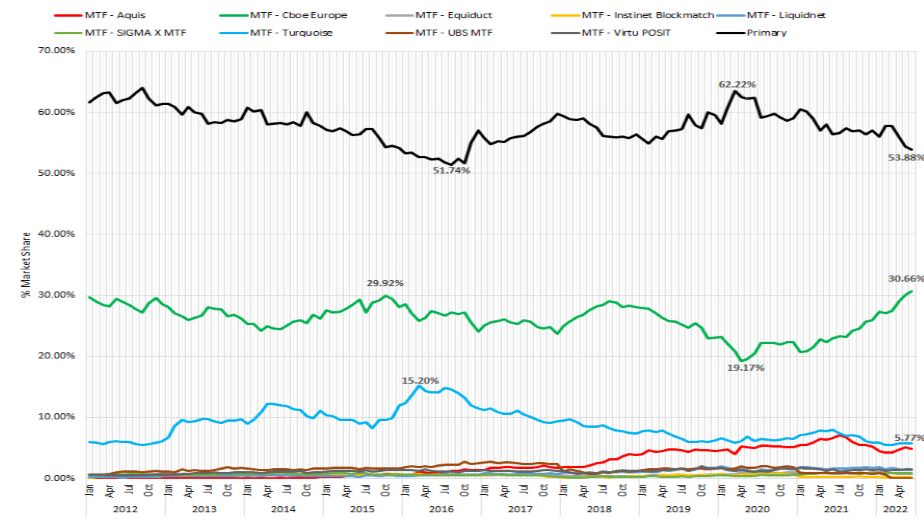

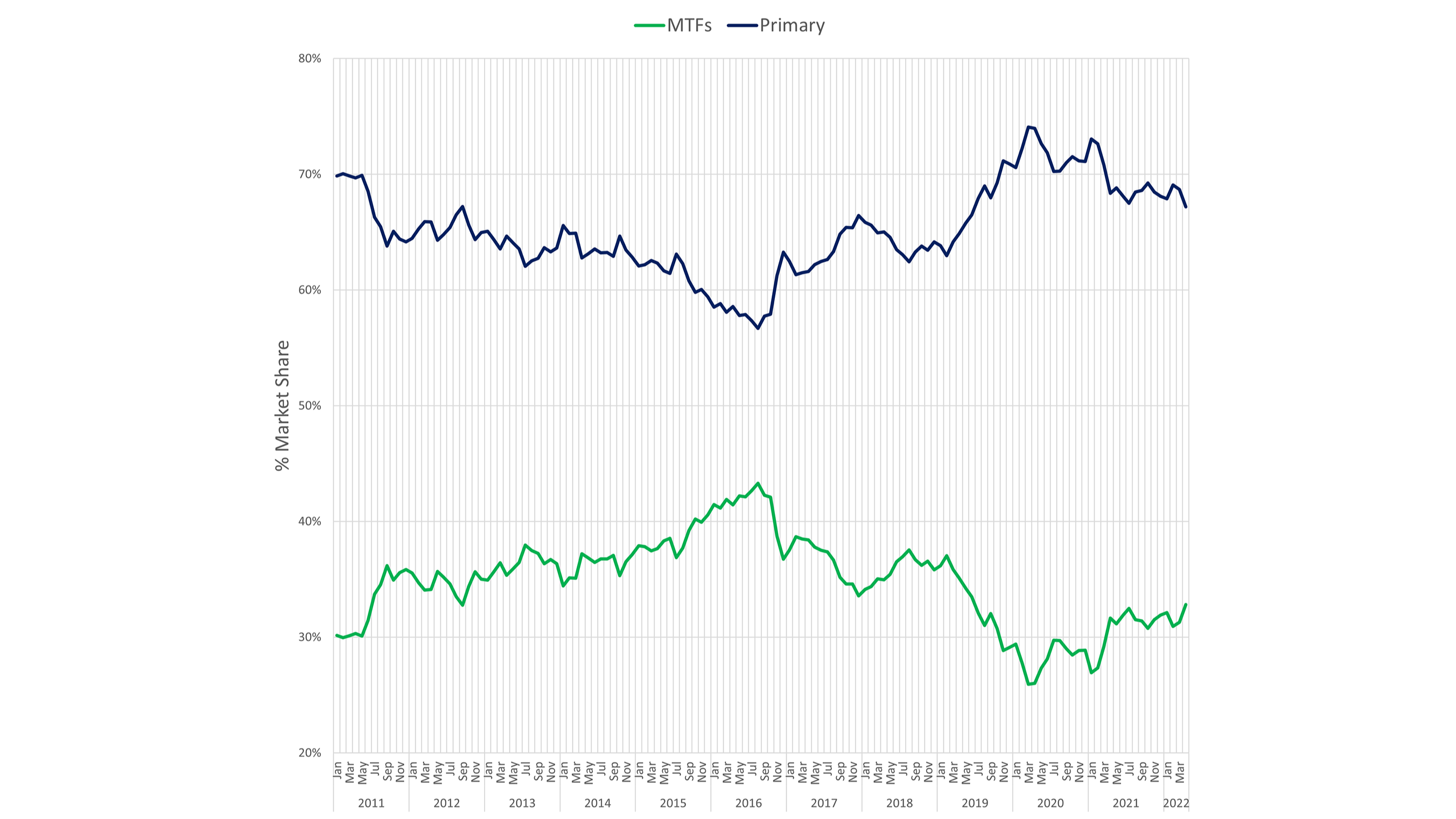

1. Robust Exchange Competition: In jurisdictions like the U.S., Canada, and European Union, competition among exchanges drives innovation, lowers costs and improves service quality. In contrast, Australia’s market structure, particularly in listings and derivatives, remains heavily concentrated.

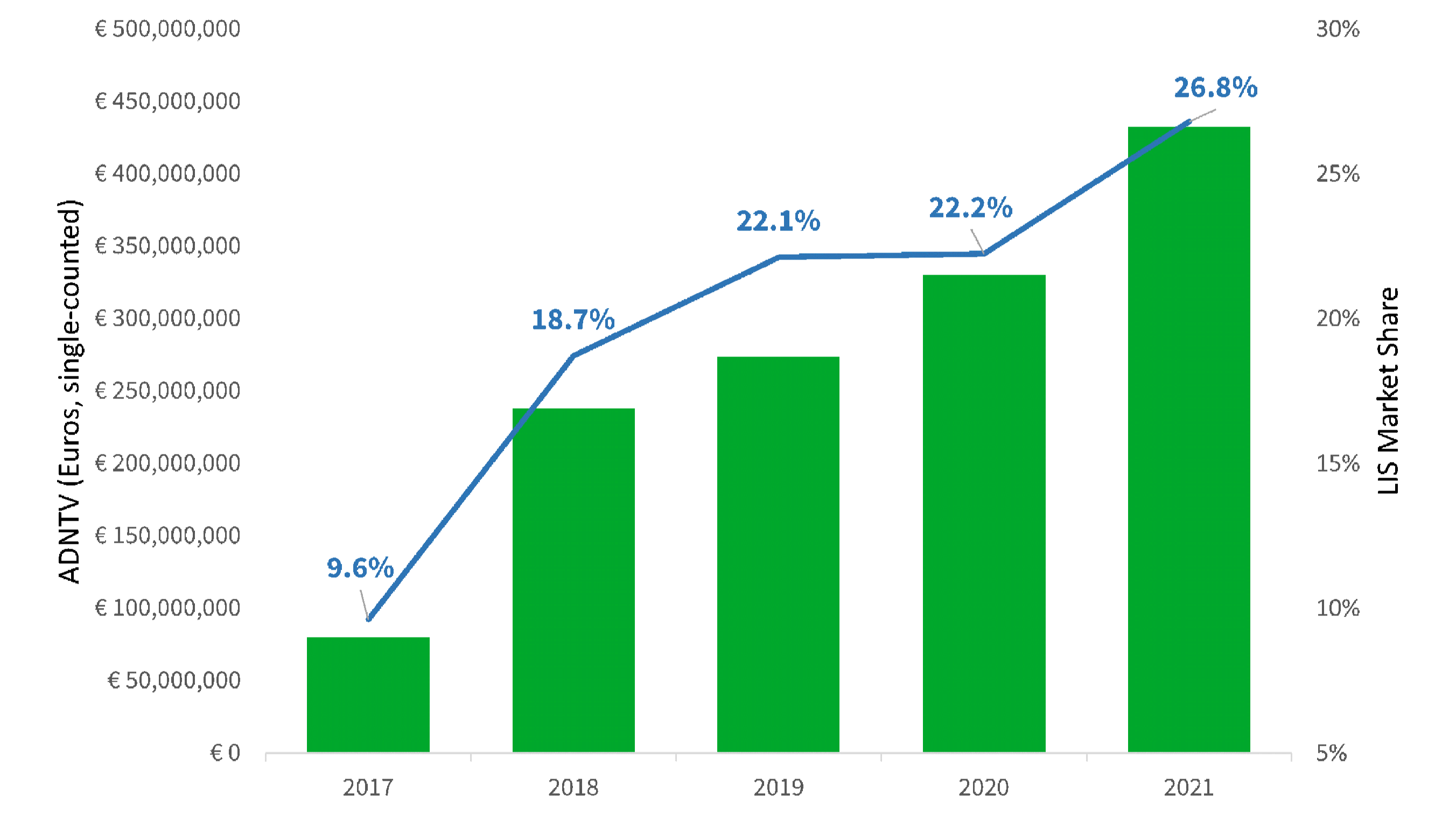

2. Vibrant Derivatives Markets: Liquid and accessible derivatives markets are essential for institutional investors to manage risk effectively. Australia’s derivatives markets, however, are often criticised for being expensive and illiquid, limiting their utility and deterring broader market participation.

3. Resilient Clearing and Settlement Infrastructure: Stable CS facilities are the backbone of any trading market. CS facility failures expose systemic risk and undermine investor confidence, which can reduce participation.

Addressing Structural Challenges

A central theme in Cboe’s submission is the need to address the structural dominance of the ASX Group. Its vertically integrated model – combining trading, clearing and settlement – creates both anti-competitive and operational risks. Unlike the US, where mutualised entities like the Depository Trust & Clearing Corporation (DTCC) and Options Clearing Corporation (OCC) operate critical infrastructure independently, Australia’s model concentrates power and limits innovation.

Cboe has called for a review by the Council of Financial Regulators (CFR) to assess whether this structure remains fit for purpose. A structurally separate, industry-owned CS facility could align commercial incentives with the broader market’s needs, fostering a more dynamic and resilient ecosystem.

A Path Forward

ASIC’s recent implementation of the CS Services Rules 2025 is a commendable step toward addressing monopoly risks in clearing and settlement. However, more work remains. The recommendations outlined in our submission provide a roadmap for reform – one that balances innovation with stability, and competition with investor protection. While it is too soon to assess the direction of the ASIC Inquiry announced on 16 June, Cboe is optimistic that some of these issues may be considered.

Embedding Regulatory Neutrality

Another barrier to competition lies in the regulatory framework itself. Many ASIC instruments are drafted in ways that favour incumbents, requiring new entrants to seek bespoke relief even after obtaining a license. This not only increases the regulatory burden but also delays innovation.

Cboe recommends that ASIC revise its instruments to be market-neutral – applying equally to all licensees regardless of their identity. This would streamline compliance, reduce administrative overhead, and support a more level playing field.

Bridging Public and Private Markets

While the focus of Cboe’s submission is on strengthening public markets, it also acknowledges the growing role of private markets. Exchange-traded funds (ETFs), for example, offer a bridge between the two, providing investors with access to private market-like exposures within a transparent and liquid structure. Continued growth and innovation in ETFs can help democratise access to alternative assets while maintaining the benefits of public market oversight.

By embracing these reforms, Australia can re-establish itself as a global leader in capital markets. It can offer investors and issuers a market environment that is not only efficient and transparent but also resilient and forward-looking.

As the global financial landscape continues to evolve, so too must Australia’s public markets. The time to act is now.

Read Cboe’s full submission for a detailed exploration of the recommendations here.

©2025 Cboe Australia Pty Ltd (ACN 129 584 667) (“Cboe Australia”). All rights reserved. Cboe is a registered trademark.

Cboe Australia is the holder of an Australian Markets Licence to operate a financial market in Australia. This information is provided for informational purposes only. It does not take into account the particular investment objectives, financial situation, or needs of any individual or entity. Under no circumstances is it to be used as a basis for, or considered as an offer to, become a participant of or trade on Cboe Australia or undertake any other activity or purchase or sell any security, or as a solicitation or recommendation of the purchase, sale, or offer to purchase or sell any security. While the information has been obtained from sources deemed reliable, neither Cboe Australia nor its licensors, nor any other party through whom the user obtains any such information: (i) makes any guarantees that it is accurate, complete, timely, or contains correct sequencing of information; (ii) makes any warranties with regard to the results obtained from its use; or (iii) shall have any liability for any claims.