Read More

By Ensi Martini

Similar to the U.S. and other global markets, the onset of the COVID-19 pandemic caused a spike in trading volumes and created lasting changes to Canadian market dynamics . However, in Canada, the timing of that market swing coincided with an amendment to the Universal Market Integrity Rules (UMIR) that impacted trading in dark venues. The change in UMIR Rule 6.6 increased the minimum size requirements for executing against resting dark liquidity at the quote. Cboe’s North American Equities Execution Consulting Team analyzed the impact of this rule change on the Canadian market and the adjustments to dark trading, as well as more recent MATCHNow enhancements.

In Canada, all Investment Industry Regulatory Organization of Canada (IIROC) regulated marketplaces and marketplace participants must adhere to all applicable IIROC rules, which includes UMIR. In particular, UMIR 6.6 (Provision of Price Improvement by a Dark Order) dictates that orders must receive price improvement to execute against a resting dark order, unless certain size requirements are met, in which case they are eligible to execute against a dark order without price improvement. Prior to February 2020, the minimum size requirement was 51 Standard Trading Units (STUs) or greater than $100,000 notional value. On February 4, 2020, the minimum size requirement was amended to 51 STUs and greater than $30,000 notional value, or greater than $100,000 notional value. Odd lot orders (less than 1 STU) are not subject to this rule and have no threshold necessary to trade at the touch in the dark.

STUs are comparable to round lots in the U.S., where lot sizes are typically 100 for most securities. Lot sizes for any given symbol in Canada dynamically shift based on the closing price of that symbol on the previous trading day, subject to certain conditions. The table below shows the various lot sizes based on price and the change in minimum size to trade at the touch in dark. Effective minimum sizes were previously based on the literal STU requirement, but the effective minimum size has increased since there is now a notional component — even if the definition still states 51 STUs. The names most affected by this change are those that trade under $1, and those that trade between $1 and $5.89 (above which, a standard 51 STUs would automatically hit the $30,000 notional requirement).

It is important to analyze the current distribution of these symbols because there are distinct impacts between sub-dollar equities and $1 or greater (also known as “senior”) equities. In 2019, before the rule change, sub-dollar securities made up 35% of Canadian executed volumes. By 2021, sub-dollar securities comprised more than 50% of volume. As a portion of notional value, however, sub-dollar securities peaked in first-quarter 2021 at 1.7% of notional value traded and more often remain under 1%. Sub-dollar trading is an increasingly important segment of the market (in part due to increased retail trading) with respect to volume, but remains negligible in terms of notional value.

Source: Cboe Global Markets

Source: Cboe Global Markets

After the rule change in February 2020, quarterly market share of pure dark venues’ (Cboe MATCHNow, NEO-D, NASDAQ-CXD, Instinet and Liquidnet) was cut in half, from around 8%. The falloff is even more steep when looking at the volume changes by month, moving from 9.21% down to 5.41% between January and February 2020. By analyzing $1 or greater and sub-dollar securities separately, our team concluded that most of this market share drop off can be attributed to sub-dollar names, which drastically declined from 10% to 3%.

The charts below further break down the market share by share price and notional value traded. More insight into the distribution of names is available for securities above a dollar, with $10-50 being the most active by notional traded, followed by $1-5. As mentioned at the beginning of this analysis, the $1-5 range is uniquely affected by the rule change, however a drop off in market share in this category was not observed. Higher priced names dominated in the notional value, which was demonstrated in the aggregate value graph above. Sub-dollar and $1-5 securities have decreased from their pre-2020 values, but not enough to make a noticeable difference.

Source: Cboe Global Markets

Source: Cboe Global Markets

Interestingly, the disconnect between the drop in volume/value and an increase in trade count is due to the fact that the minimum size does not apply to orders less than one STU. This part of the definition did not change from before, but with the increased threshold for dark trading at the touch, flow naturally shifted to odd lots, which are still allowed to execute at the quote. Consequentially, the percentage of odd lot trades has soared in that same time frame. In sub-dollar equities, the percentage of trades done for less than one STU climbed from 15% in first-quarter 2019 to 27% in first-quarter 2021. Clearly, there is still demand for at-the-quote dark trading.

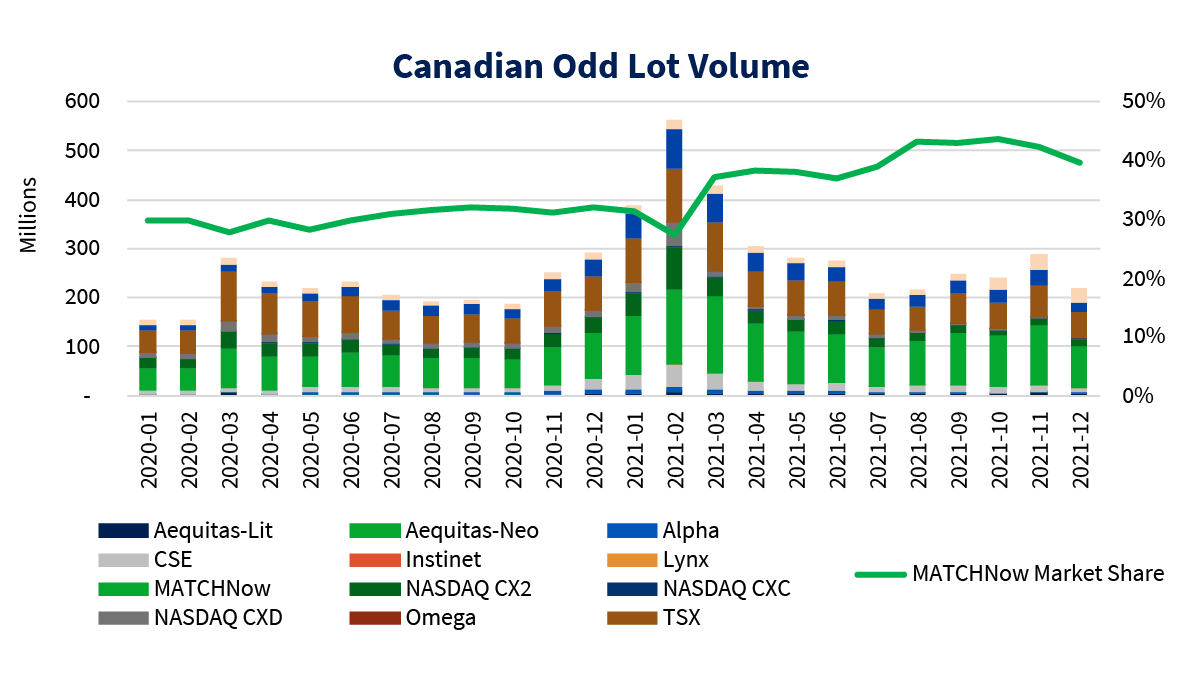

Source: Cboe Global Markets

When it comes to overall odd lot volume, Cboe MATCHNow was the clear leader in Canadian market share in 2021. This growth in market share corresponds with the increase in odd lot trade count in the graph above, as odd lots are free to trade on MATCHNow.

Source: Cboe Global Markets

A key indicator of market quality is average trade volume and value, illustrated in the two charts below. Prior to the rule change, the average trade sizes for both lit and dark venues were in line with one another. However, in February and March 2020 (shortly after the rule change and the beginning of the volume spike), these measures diverged and dark average trade sizes (both volume and notional value) dropped below lit venue averages. After the rule change, the average share trade size in dark venues was more than halved, down from approximately 600 shares to approximately 200 shares.

Notional value has also dropped off in dark trading, but the effect is much more amplified for sub-dollar equities, which declined 85% between first-quarter 2019 and third-quarter 2021, from about 1,300 to about 200. Lit venues dipped slightly, then recovered in subsequent quarters. This lasting divide suggests a cause deeper than temporary changes in market activity – participants have adjusted for the paradigm shift.

Source: Cboe Global Markets

Source: Cboe Global Markets

The charts below show changes in average spreads and displayed order sizes for four Canadian indices: TSX 60, TSX Comp, TSX Venture and Canada/U.S. Interlisted. These indices represent different components of the Canadian market and the TSX Venture Index highlights the impact to sub-dollar equities. The chart below shows the quoted spreads for the equities in the various indices. Outside of the pandemic-induced volatility in spring 2020, overall spreads have tightened since pre-pandemic levels, with the biggest improvement in the TSX Venture Index names.

Source: Cboe Global Markets

Display sizes, on the other hand, have continued to increase slightly in all indices, except the TSX Venture Index, which declined in display size. The displayed sizes of Venture equities have decreased by almost half from the pre-rule change 2020 averages.

Source: Cboe Global Markets

Source: Cboe Global Markets

The new constraints for dark trading coincided with an increase in the use of block trading mechanisms in dark trading, specifically conditional orders. During this timeframe, Cboe’s MATCHNow conditionals destination has seen increased use and volume growth. The block-sized liquidity available ensures higher quality fills and a reliable execution environment. With the February 2022 upgrade to the Cboe technology platform, MATCHNow conditionals now allow at-the-touch trading in addition to midpoint. Additionally, the average trade size of MATCHNow conditionals is significantly greater than overall market execution sizes. In December 2021, for example, average trade size was 15,402 by volume and $404,493 by notional value.

Due to increased demand for conditional trading, MATCHNow recently enhanced its conditionals offering to enable conditional orders to interact with MATCHNow firm orders through the new Willing-To-Trade feature. This has expanded conditional block trading opportunities to most MATCHNow order flow. The new feature can be enabled at the port level for added efficiency, instantly providing access to conditional block trading without any additional client modifications.

With the introduction of Willing-To-Trade, conditionals hit new volume, notional value and trade count records in November. The graph below illustrates conditionals volume surpassing 20 million for the first time, and average trade sizes hovering around 15,000. Willing-To-Trade alone already contributes 2.8 million shares, making up about 15% of conditional orders.

Source: Cboe Global Markets

Cboe MATCHNow enhanced its conditional orders innovation with the roll out of Cboe BIDS Canada. This innovation enables sponsored buy-side clients to engage with existing MATCHNow conditional flow. This innovation will enable sponsored buy-side clients to engage with existing MATCHNow conditional flow. Market participants affected by the UMIR rule change they may find that Conditionals help improve execution in this new landscape.

The chart below shows the percentage of conditional trades that are among the largest in volume for that symbol, on that day. Excluding intentional crosses, historically, it is extremely likely that a conditionals print (which has a size requirement on orders) will be among the top 1% of all activity for that symbol. In the past two years, there have been several instances where conditionals prints make up the majority of top block trades in a security.

Source: Cboe Global Markets

Taking the data we analyzed into consideration, it appears that the UMIR 6.6 rule change did not have a material impact on overall Canadian market quality, outside of an increase in odd lot trading and a decline in dark venue market share. This analysis does not take into consideration any potential changes to trading cost, including differences in trading fees and trading caps in dark and lit venues for market participants. The migration of order flow from dark to lit markets has led to tighter quotes in sub-dollar equites, but there has also been a decline in overall sub-dollar equities displayed size. Dark markets have recently started claw back the lost market share. We are confident that the continued adoption of conditional trading, as well as innovations in the space, such as Cboe MATCHNow’s new Willing-To-Trade feature and the recent launch of Cboe BIDS Canada, will continue to provide value to our clients and subscribers.

We encourage market participants that were impacted by the rule change to reach out to the Cboe MATCHNow team to discuss conditionals and related products that can help mitigate impact and exposure.