US Elections Day Risk Rises as Trump Gains in the Polls

Ed Tom

▬

October 24, 2024

Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- Volatility traders flattened the S&P-500® Index skew following OPEC’s lowered revision for oil demand growth (its 3rd consecutive downward revision), shaving 1 volpt of geopolitical risk premium off of the VIX® Index. Nonetheless, skew remains steep (84th percentile highs) and we estimate that the current VIX® Index level of 18 still embeds a total of 3.5pts of geopolitical risk premium (i.e., if MidEast tensions were to dissipate entirely, VIX would fall to 14.5).

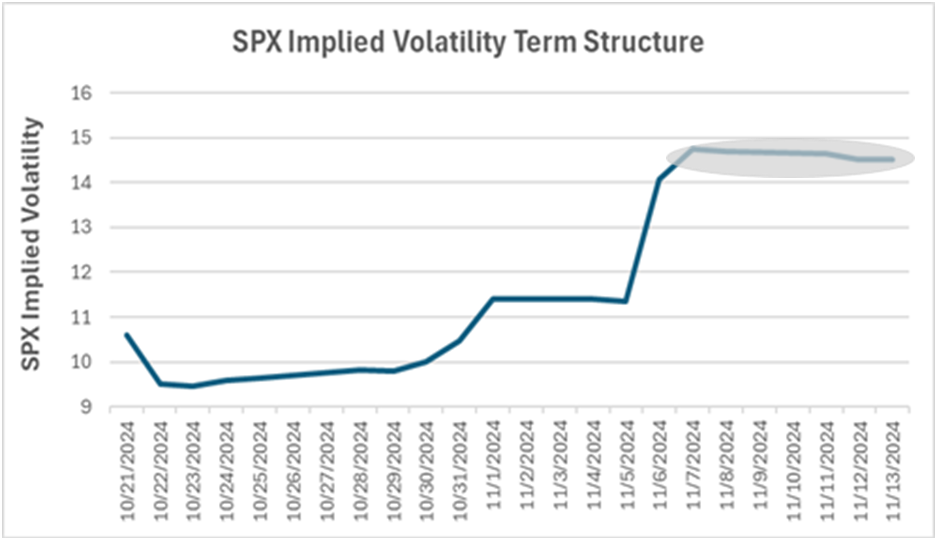

- The US Elections Day premium embedded into Nov 6th vs Nov 5th expiry S&P® options has widened by an additional ¼ point to 2.73 wk/wk as Trump gains in the polls. We believe this direct relationship between elections risk and Trump’s poll gains reflects the possibility of (Jan 6th style) protests if there is a disconnect between the polls and US election outcome.

- The post-Elections volatility premium representing the risk of a contested election, however, has declined on Trump poll gains. Specifically, the length of time accorded to resolve a contested election has shortened by 50% and is now only reflected in the volatility term structure for one-week post-Elections (vs. 2 weeks at the beginning of October).

Chart: US Elections Day Event Risk Higher, Risk of Contested Election Lower on Trump Poll Gains

Source: Cboe

[Download Full Report Here]

[Subscribe Here]