SPX® Intraday Volatility Highest Since 2008 on Tariff U-Turn

Mandy Xu

▬

April 14, 2025

Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- While equity and credit volatilities fell last week on Trump’s tariff U-turn, FX, gold, oil, and interest rate volatilities all increased. Notably, both US Treasuries and US Dollar sold off, with VIXTLT jumping over 60 pts to a high of 190. TLT skew, which had been inverted since Feb as growth concerns weighed on yields, steepened significantly last week with puts now trading at a premium to calls (i.e. positioning for yields to go even higher).

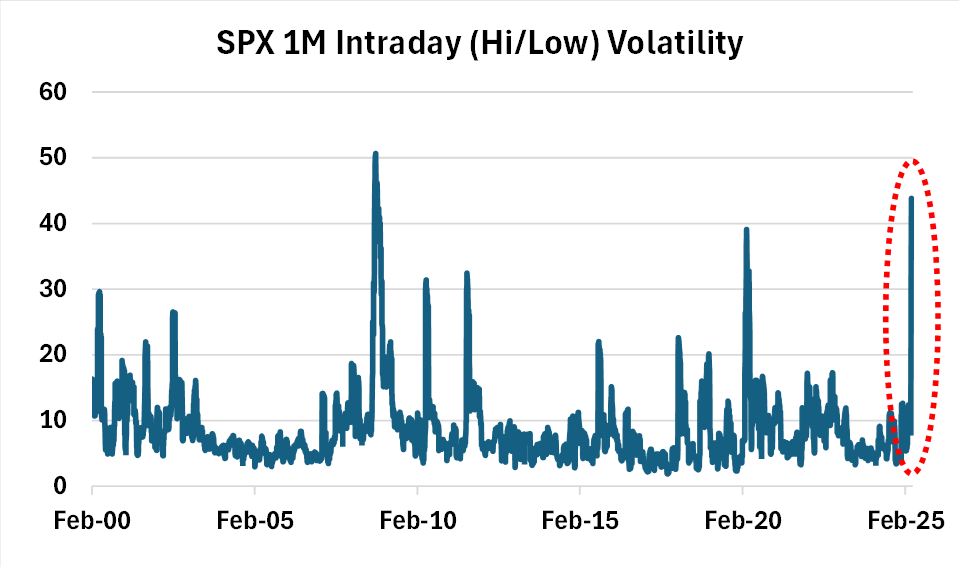

- SPX 1M ATM vol fell 5 pts to 32.5% even as realized volatility continued to rise – especially intraday volatility. As the chart below shows, SPX intraday (hi/low) volatility almost doubled last week to 44%, exceeding the 2020 covid highs and is now reaching levels last seen during the depth of the 2008 GFC (VIX traded 80+ both in 2008 and 2020).

- As focus now shifts to potential tariffs on the Tech sector, it’s notable that SPX index (cap-weighted) is realizing significantly higher volatility than SPW (S&P Equal Weight Index), in large part due to the high concentration of large-cap Tech. The volatility differential between the two is at its highest since 2001.

- Cboe is launching options on the equal-weight index today (ticker: SPEQX, with 1/10th the size of SPW). See more here.

Chart: SPX Intraday Volatility Highest Since 2008 GFC

Source: Cboe

[Download Full Report Here]

[Subscribe Here]