Election Risk Premium Continues to Widen into Elections Week

Ed Tom

▬

October 28, 2024

Link to Report: Macro Volatility Digest

WHAT STANDS OUT:

- The VIX® Index traded sticky-strike (i.e., in line with the pre-established skew) for most of last week – including in response to last Wednesday’s -1% S&P® Index pullback on lower than expected MoM Existing Home Sales. In this context, last Friday’s volatility action was particularly surprising with both the VIX and VVIX Indexes rising 1.25 pts and 7.7 pts to 20 and 118 respectively despite the fact that the S&P 500 was virtually unchanged for the day (S&P -3 bps). This is due to a steepening in the skew gradient coming into the weekend. Although we believe that the steepened skew reflects a combination of positioning for both geopolitical uncertainties coming into the weekend and earnings uncertainties for 3 Mag 7’s, we infer from Friday’s rise in implied correlations and VVIX (both more macro sensitive measures) that MidEast tensions was responsible for a greater percentage of Friday’s additional VIX risk premium. If that is indeed the case, we should see the VIX underperform skew this week.

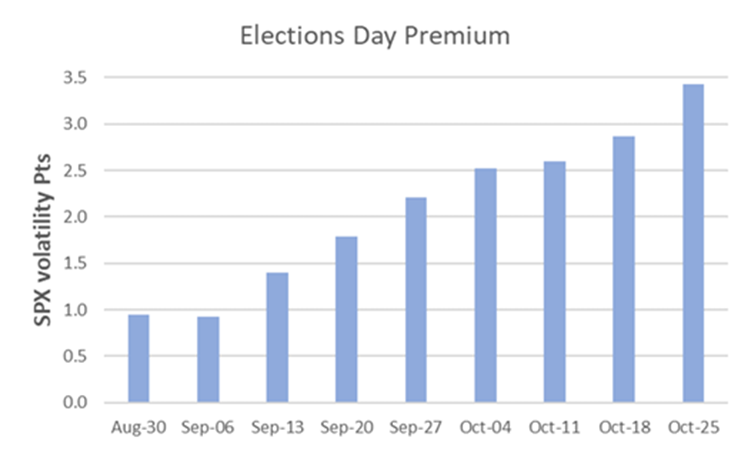

- With a week left to go till Election Day, Nate Silver currently sees a steady momentum shift towards Trump (Trump slightly ahead in the battleground states of NC, AZ, GA, and PA. We continue to observe a positive correlation between Trump poll momentum and increased Elections Day risk premium along the volatility term structure. (Nov 6 expiries current trade at a 3.43 vol pt premium vs Nov 5, a widening of 1.22 vol pts from a month ago.)

Chart: Elections Day Premium (Nov 6 – Nov 5 ATM SPX Vols) Continues to Widen Heading into Elections Week

Source: Cboe

[Download Full Report Here]

[Subscribe Here]