Inside Volatility Trading: Mercury and Market Retrograde

Kevin Davitt

▬

February 15, 2022

The moments are mine, if I can just seize the day

But then I forget what it is that I meant to say

I try to hold on, but never too tight

The hours go by until Mercury comes out at night

-Anastasio/Marshall

Celestial Connections

Astrology tries to glean useful information by studying celestial objects. While I do not put much stock in the pseudoscience, according to astrology, there are three or four periods during a calendar year when Mercury is in retrograde. During “retrograde” periods, the planet Mercury appears to move backwards. Astrological subscribers believe that communication and technology can be impaired when Mercury is in retrograde.

This isn’t an attempt to dismiss the study of objects in the sky. In many ways, market participants behave similarly and attempt to discern trends and identify opportunity based on specific relationships. For example, using price-to-earnings ratios, analyzing the impact of interest rates on U.S. equities, or examining the relative performance of growth and value stocks.

Participants continuously compare one variable relative to another.

Some unusual things have occurred in capital markets lately. What are the shifting relationships potentially saying about the future?

Technology (Impaired)

Perhaps it was in the stars, but the technology sector has been particularly distressed of late. The chart below plots the performance of the Cboe Select Sector Technology Index over the past six months. From late December to late January, this technology barometer declined by more than 14%. By comparison, the S&P 500 Index fell by 9.8% over a very similar time frame.

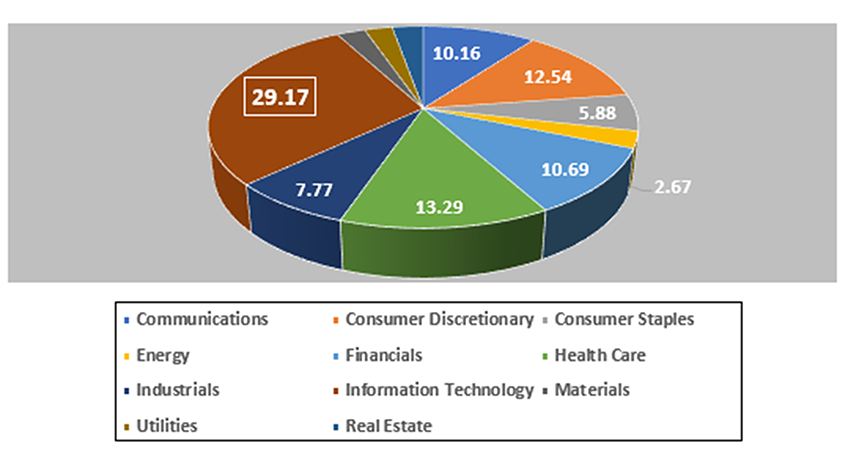

Every constituent stock in the S&P 500 Index can be broken down into one of eleven sector categories. Each sector has its own weight within the index. The Technology sector is by far the largest. Below is a breakdown of sector weights as of the end of 2021:

Cboe Technology Select Sector Performance Over 6 Months

Source: Cboe Global Markets

Every constituent stock in the S&P 500 Index can be broken down into one of eleven sector categories. Each sector has its own weight within the index. The Technology sector is by far the largest. Below is a breakdown of sector weights as of the end of 2021:

S&P 500 Index Sector Weights

Source: S&P Dow Jones Indices and Cboe Global Markets

The weightings change over time and the influence of technology has steadily increased. For example, at the end of 2018, technology accounted for 20.12% of the S&P 500 Index. Now, tech makes up 29.17% of the index.

In 2022, the second most influential group is health care at 13.29%. Based on current weights, technology stocks have more than double the impact of health care names in the S&P 500 Index. Naturally, the relationship between technology stocks and the S&P 500 Index is highly correlated.

As goes General Motors, so goes America… has evolved into: As goes Apple, Microsoft, Amazon, and Alphabet, so goes the U.S. economy. The current version of this saying is a generalization but is reflective of the weightings of technology stocks within the S&P 500 Index.

Interest Rates

The price of government bonds, particularly those with shorter maturities have declined considerably over the past seven months. The price and yield for a bond move in opposite directions; when bond prices fall, yields are increasing. There’s been a significant move in bond prices and respective yields.

For example, in mid-June 2020, the yield on the U.S. 2-year treasury was 0.17%. As of February 11, the U.S. 2-year yield was 1.60%. Longer-dated bond (10Y, 20Y, 30Y maturities) yields have also increased, but not with the same velocity as the short end of the yield curve.

The relationship between U.S. Treasury (UST) yields with different maturities is a scrutinized data point. Individuals and institutions often choose to borrow money (use credit) to finance their lifestyle or grow business. Many interest rates from mortgage and credit card rates to overnight lending rates between banks are sensitive to the U.S. yield curve. The UST term structure has been flattening since mid-2021. Many argue that it’s only a matter of time before the yield curve inverts. Historically, there have been recessions which have occurred when there have been yield curve inversions.

10 Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity

Source: St. Louis Fed

In fact, a dynamic where short-dated bond yields are higher than longer-dated bonds can reinforce an economic slowdown. The cost of capital is perhaps the most important component for evaluating so many other market relationships. Any investment that involves borrowed money becomes more expensive when the cost of capital increases. More is spent on interest payments. Higher rates incentivize saving (as opposed to consumption) which impacts businesses and the economy as a whole.

Rates & Earnings, An Example

Interest rates have a meaningful impact on the value of future earnings for individual equities. Let’s explore this relationship.

The return from an equity could arguably be broken down into a few components. They include:

- Yield

- Growth

- Changes in valuation

Ultimately a company’s stock price and valuation may be reflective of its future cash flows discounted by some interest rate. That gives you a net-present value of future earnings. From that you can extrapolate a valuation.

A basic discounted cash flow model is below:

Cash Flow Model

Let’s assume that Company A expects to receive a single cash flow of $1000 ten years from now. That’s our numerator. The interest rate is our denominator, and we use two values to compare. In one example we’ll assume interest rates at 0.50%. In the second situation, we’ll assume 5.0% interest rates. The output is the net-present value of that future cash flow.

- Present value of $1000 assuming 0.50% = $951.35

- Present value of $1000 assuming 5.0% = $613.90

The difference of $337.45 for the net present value (NPV) of $1000 in the future is entirely a function of higher interest rates. In other words, the NPV of future revenue is 35% lower because of the higher discount rate. The relationship between the cost of capital and future earnings can be significant!

Now, how does this relate to share price and valuation?

Valuation, An Example

We’re going to build on our above example and introduce a couple of assumptions. The goal is to arrive at a hypothetical share price/valuation for Company A.

Valuation is straight forward when you know stock price and shares outstanding.

For our example, we’ll solve for earnings and then apply a typical P/E ratio for a technology company to give us a share price. The P/E ratio for many IT stocks is ~30. In other words, their share price is typically about 30 times annual earnings.

We showed that the value of future revenue (cash flows) is reduced when interest rate assumptions increase. To arrive at a hypothetical earnings number, we must make an assumption about the cost of goods sold (COGS). The COGS is the sum of what it costs Company A to make and deliver their product.

We’ll keep the COGS figure constant across examples but note that the COGS would likely be higher in a higher interest rate environment.

Let’s say that the COGS works out to $400 no matter the interest rate environment. We subtract this amount from the NVP of Income to find our earnings value.

Calling attention to the right side of the table above, you’ll notice that earnings are significantly lower when rates are higher because our discounted revenue value is lower.

Our example is simplified, but this dynamic has likely played out across U.S. equity markets for months. Higher rates have likely put downward pressure on the value of future earnings and valuations, most notably in the growth focused tech sector.

Let’s tie this all together with a hypothetical share price. In this next table, we use the earnings from the first visual and assume Company A only has 100 shares of outstanding stock. That makes calculating our earnings per share very easy. We take the (total) earnings number from above and divide by shares outstanding (100). Finally, we apply the “average” P/E multiple for tech companies – 30 -- to arrive at a hypothetical share price. Notice the impact of rates on share price.

The relationship between interest rates, earnings, and potential valuation/share prices is becoming clearer. Higher rates reduced the value of future earnings, and our stock price is 60% lower as a result. Portfolios with significant exposure to growth companies have been in retrograde.

Growth

Growth rates and future earnings are inextricably connected. In general, technology companies are focused on scale. The pursuit of scale tends to be internal as well as external. Tech companies often need to increase their user base to generate higher incremental revenue (internal). Their products often allow end users to do more with less (external).

Examples:

- ETSY allows crafters to reach a much broader market of potential buyers than someone dependent on a brick-and-mortar store in one physical market.

- TWTR allows Elon Musk to “communicate” with his 73 million followers with little friction.

Companies like ETSY and Twitter can be dependent on user base growth for future earnings.

ETSY Year-Over-Year (YoY) Growth By Quarter 2015 - 2021

Source: MacroTrends

ETSY is an example of a company that benefitted from the pandemic. You can see the huge revenue growth for the firm in 2020. The growth narrative boosted share price, but ultimately that growth wasn’t sustainable.

Low interest rates allowed growth companies to pursue “scale” with cheap dollars. The interest rate backdrop is changing, and growth stock prices have likely reflected the shifting relationship.

There are a wide variety of tech/growth stock charts that look nearly identical to ETSY’s; the given growth company’s stock moves higher between April 2020 and late 2021 followed by a 50-60% since early November.

ETSY Performance MID-2019-Present

Source: Cboe LiveVol Pro

Cathy Wood’s ARKK ETF, which primarily invests in technology companies, is a broader example. The fund is down 24% YTD (reference $71.50) and the average ARKK component has lost 63% of its value from 2021 highs.

Value

Value companies often command much lower price to earnings ratios. Investors aren’t normally willing to pay the same multiple for future earnings in companies that aren’t expected to grow rapidly. Value companies often pay out a dividend stream which makes them more attractive during “risk off” or low growth periods.

Over the past two months, there’s been a noticeable outperformance on the part of value stocks relative to growth. The story over the past decade, however, is quite the opposite. Growth companies have dominated during a decade with historically low rates. Furthermore, the pandemic drove demand for IT products that facilitated the “new normal” work environment.

It remains to be seen whether we’re experiencing a “sea change” where value stocks lead for years or not. The last period of significant outperformance on the part of value took place between mid-2003 and late 2007.

Below is a chart that tracks the Fed Funds rate between 2003 and 2010. Value stocks started to outperform when the Federal Reserve (under Greenspan) communicated their intent to tighten policy. Value fell out of favor in the middle of 2007 following a UST yield curve inversion and looser monetary policy (under Bernanke).

Fed Funds Growth Rate 2003-2010

Source: MacroTrends & Cboe Options Institute

So, there’s been a historical relationship between interest rates and the relative appeal of growth or value stocks. In general, growth stocks are more attractive in a declining interest rate environment. Value stocks have a history in which they often outperform during rate hike cycles. Interest rates are like the sun- at the center of this investment universe.

Here & Now

So far, 2022 has looked quite different when compared to last year. The S&P 500 Index fell nearly 10% from highs. Compare that to last year when the largest peak to trough drawdown for the S&P 500 Index was 5.2%. The pullback in the Nasdaq 100 Index was even more pronounced at 15.5%. The Nasdaq 100 is technology (growth) focused and the marketplace has been repricing the risk of rising rates. Tech stocks have been more sensitive, which is similar to the dynamic observed between 2003 and late 2007.

The S&P 500 Index has experienced meaningful dispersion with respect to sector performance. In January, energy advanced by 18.8% whereas consumer discretionary fell by 9.5%. Historically performance spreads of that magnitude have only been observed in “high vol” markets.

S&P 500 Index Sector Spread

Source: S&P Dow Jones Research

Finally, in late January/early February of last year, market participants drove the Cboe Total Put/Call ratio to record lows. Calls, particularly well out-of-the-money calls were in huge demand. In early February of this year the total put volume relative to calls is at the highest levels since April of 2020. Put options appear to be back in vogue. Market participants seem more interested in downside protection than upside exposure.

Still new to the options market or simply interested in smaller exposure? Cboe is excited to introduce Nanos. These first-of-their-kind options have a one-multiplier, are cash-settled, and are available for trading on the S&P 500 Index in March 2022.

Big picture, the relationships between distinct data points can be informative. I didn’t notice any unusual communication or technological issues when Mercury was in retrograde. We have, however, explored the evolving relationship between the S&P 500 Index, the component sectors, and the impact of interest rates on futures earnings and market rotations.

We’ll see what’s in store for the Fed Funds rate on March 16.

As for the next time when Mercury is in retrograde, you’ll have to wait until May 10.

Industry News

- Markets Media: ETFs in Europe Gathered a New Monthly Record

- Markets Media: MEMX to Charge for Market Data

- Markets Media: SETL and Digital Asset Create Regulated Network for Tokens

- The Trade: US buy-side warily eyeing changes to payment for order flow, finds report

- Risk.net: Rough volatility moves to exotic frontiers

Events

- February 23: Options Insights Webinar Series

- February 25-26: STA Florida

Volatility411

Get This Newsletter Sent to Your Inbox

Get the Inside Volatility Trading newsletter directly in your inbox by signing up here.

There are important risks associated with transacting in any of the Cboe Company products discussed here. Before engaging in any transactions in those products, it is important for market participants to carefully review the disclosures and disclaimers below.

General

The information provided is for general education and information purposes only. No statement provided should be construed as a recommendation to buy or sell a security, future, financial instrument, investment fund, or other investment product (collectively, a “financial product”), or to provide investment advice.

In particular, the inclusion of a security or other instrument within an index is not a recommendation to buy, sell, or hold that security or any other instrument, nor should it be considered investment advice.

Options

Options involve risk and are not suitable for all market participants. Prior to buying or selling an option, a person should review the Characteristics and Risks of Standardized Options (ODD) , which is required to be provided to all such persons. Copies of the ODD are available from your broker or from The Options Clearing Corporation, 125 S. Franklin Street, Suite 1200, Chicago, IL 60606.

Trading FLEX options may not be suitable for all options-qualified market participants. FLEX options strategies only should be considered by those with extensive prior options trading experience.

Uncovered option writing is suitable only for the knowledgeable market participant who understands the risks, has the financial capacity and willingness to incur potentially substantial losses, and has sufficient liquid assets to meet applicable margin requirements. In this regard, if the value of the underlying instrument moves against an uncovered writer's options position, the writer may incur large losses in that options position and the participant’s broker may require significant additional margin payments. If a market participant does not make those margin payments, the broker may liquidate positions in the market participant’s account with little or no prior notice in accordance with the market participant’s margin agreement.

Futures

Futures trading is not suitable for all market participants and involves the risk of loss, which can be substantial and can exceed the amount of money deposited for a futures position. You should, therefore, carefully consider whether futures trading is suitable for you in light of your circumstances and financial resources. You should put at risk only funds that you can afford to lose without affecting your lifestyle.

For additional information regarding the risks associated with trading futures and security futures, see respectively the Risk Disclosure Statement set forth in Appendix A to CFTC Regulation 1.55(c) and the Risk Disclosure Statement for Security Futures Contracts.

VIX® Index and VIX® Index Products

The Cboe Volatility Index® (known as the VIX Index) is calculated and administered by Cboe Global Indices, LLC. The VIX Index is a financial benchmark designed to be a market estimate of expected volatility of the S&P 500® Index, and is calculated using the midpoint of quotes of certain S&P 500 Index options as further described in the methodology, rules and other information here .

VIX futures and Mini VIX futures, traded on Cboe Futures Exchange, LLC, and VIX options, traded on Cboe Options Exchange, Inc. (collectively, “VIX® Index Products”), are based on the VIX Index. VIX Index Products are complicated financial products only suitable for sophisticated market participants.

Transacting in VIX Index Products involves the risk of loss, which can be substantial and can exceed the amount of money deposited for a VIX Index Product position (except when buying options on VIX Index Products, in which case the potential loss is limited to the purchase price of the options).

Market participants should put at risk only funds that they can afford to lose without affecting their lifestyles.

Before transacting in VIX Index Products, market participants should fully inform themselves about the VIX Index and the characteristics and risks of VIX Index Products, including those described here. Market participants also should make sure they understand the product specifications for VIX Index Products ( VIX futures , Mini VIX futures and VIX options ) and the methodologies for calculating the underlying VIX Index and the settlement values for VIX Index Products. Answers to questions frequently asked about VIX Index products and how they are settled is available here .

Not Buy and Hold Investment: VIX Index Products are not suitable to buy and hold because:

- On their settlement date, VIX Index Products convert into a right to receive or an obligation to pay cash.

- The VIX Index generally tends to revert to or near its long-term average, rather than increase or decrease over the long term.

Volatility: The VIX Index is subject to greater percentage swings in a short period of time than is typical for stocks or stock indices, including the S&P 500 Index.

Expected Relationships: Expected relationships with other financial indicators or financial products may not hold. In particular:

- Although the VIX Index generally tends to be negatively correlated with the S&P 500 Index – such that one tends to move upward when the other moves downward and vice versa – that relationship is not always maintained.

- The prices for the nearest expiration of a VIX Index Product generally tend to move in relationship with movements in the VIX Index. However, this relationship may be undercut, depending on, for example, the amount of time to expiration for the VIX Index Product and on supply and demand in the market for that product.

- Mini VIX futures contracts trade separately from regular-sized VIX futures, so the prices and quotations for Mini VIX futures and regular-sized VIX futures may differ because of, for example, possible differences in the liquidity of those markets.

Final settlement Value: The method for calculating the final settlement value of a VIX Index Product is different from the method for calculating the VIX Index at times other than settlement, so there can be a divergence between the final settlement value of a VIX Index Product and the VIX Index value immediately before or after settlement. (See the SOQ Auction Information section here for additional information.)

Exchange Traded Products ("ETPs")

Cboe does not endorse or sell any ETP or other financial product, including those investment products that are or may be based on a Cboe index or methodology or on a non-Cboe index that is based on investment products trading on a Cboe Company exchange (e.g., VIX futures); and Cboe makes no representations regarding the advisability of investing in such products. An investor should consider the investment objectives, risks, charges, and expenses of these products carefully before investing. Investors also should carefully review the information provided in the prospectuses for these products.

Investments in ETPs involve risk, including the possible loss of principal, and are not appropriate for all investors. Non-traditional ETPs, including leveraged and inverse ETPs, pose additional risks and can result in magnified gains or losses in an investment. Specific risks relating to investment in an ETP are outlined in the fund prospectus and may include concentration risk, correlation risk, counterparty risk, credit risk, market risk, interest rate risk, volatility risk, tracking error risk, among others. Investors should consult with their tax advisors to determine how the profit and loss on any particular investment strategy will be taxed.

Cboe Strategy Benchmark Indices

Cboe Strategy Benchmark Indices are calculated and administered by Cboe Global Indices, LLC as described in the methodologies, rules and other information available here using information believed to be reliable, including market data from exchanges owned and operated by other Cboe Companies.

Strategy Benchmark Indices are designed to measure the performance of hypothetical portfolios comprised of one or more derivative instruments and other assets used as collateral. Past performance is not indicative of future results. Strategy Benchmark Indices are not financial products that can be invested in directly, but can be used as the basis for financial products or managing portfolios.

The actual performance of financial products such as mutual funds or managed accounts can differ significantly from the performance of the underlying index due to execution timing, market disruptions, lack of liquidity, brokerage expenses, transaction costs, tax consequences and other considerations that may not be applicable to the subject index. Index and Benchmark Values Prior to Launch Date

Index and benchmark values for the period prior to an index’s launch date are calculated by a theoretical approach involving back-testing historical data in accordance with the methodology in place on the launch date (unless otherwise stated). A limitation of back-testing is that it reflects the theoretical application of the index or benchmark methodology and selection of the index’s constituents in hindsight. Back-testing may not result in performance commensurate with prospective application of a methodology, especially during periods of high economic stress in which adjustments might be made. No back-tested approach can completely account for the impact of decisions that might have been made if calculations were made at the same time as the underlying market conditions occurred. There are numerous factors related to markets that cannot be, and have not been, accounted for in the preparation of back-tested index and benchmark information.

Taxes

No Cboe Company is an investment adviser or tax advisor, and no representation is made regarding the advisability or tax consequences of investing in, holding or selling any financial product. A decision to invest in, hold or sell any financial product should not be made in reliance on any of the statements or information provided. Market participants are advised to make an investment in, hold or sell any financial product only after carefully considering the associated risks and tax consequences, including information detailed in any offering memorandum or similar document prepared by or on behalf of the issuer of the financial product, with the advice of a qualified professional investment adviser and tax advisor.

Under section 1256 of the Tax Code, profit and loss on transactions in certain exchange-traded options and futures are entitled to be taxed at a rate equal to 60% long-term and 40% short-term capital gain or loss, provided that the market participants involved and the strategy employed satisfy the criteria of the Tax Code. Market participants should consult with their tax advisors to determine how the profit and loss on any particular option or futures strategy will be taxed. Tax laws and regulations change from time to time and may be subject to varying interpretations.

General

Past performance of an index or financial product is not indicative of future results.

Brokerage firms may require customers to post higher margins than any minimum margins specified.

No data, values or other content contained in this document (including without limitation, index values or information, ratings, credit-related analyses and data, research, valuations, strategies, methodologies and models) or any part thereof may be modified, reverse-engineered, reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of Cboe.

Cboe does not guarantee the accuracy, completeness, or timeliness of the information provided. THE CONTENT IS PROVIDED “AS IS” WITHOUT WARRANTY OF ANY KIND, EITHER EXPRESS OR IMPLIED, INCLUDING, WITHOUT LIMITATION, ANY WARRANTY WITH RESPECT MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE.

Hypothetical scenarios are provided for illustrative purposes only. The actual performance of financial products can differ significantly from the performance of a hypothetical scenario due to execution timing, market disruptions, lack of liquidity, brokerage expenses, transaction costs, tax consequences and other considerations that may not be applicable to the hypothetical scenario.

Supporting documentation for statements, comparisons, statistics or other technical data provided is available by contacting Cboe at www.cboe.com/Contact .

The views of any third-party speakers or third-party materials are their own and do not necessarily represent the views of any Cboe Company. That content should not be construed as an endorsement or an indication by Cboe of the value of any non-Cboe financial product or service described.

The inclusion of research not conducted or explicitly endorsed by Cboe should not be construed as an endorsement or indication of the value of that research.

Trademarks and Intellectual Property

Cboe®, Cboe Global Markets®, Bats®, BIDS Trading®, BYX®, BZX®, Cboe Options Institute®, Cboe Vest®, Cboe Volatility Index®, CFE®, EDGA®, EDGX®, Hybrid®, LiveVol®, Silexx® and VIX® are registered trademarks, and Cboe Futures ExchangeSM, C2SM, f(t)optionsSM, HanweckSM, and Trade AlertSM are service marks of Cboe Global Markets, Inc. and its subsidiaries. Standard & Poor's®, S&P®, S&P 100®, S&P 500® and SPX® are registered trademarks of Standard & Poor's Financial Services LLC and have been licensed for use by Cboe Exchange, Inc. Dow Jones®, Dow Jones Industrial Average®, DJIA® and Dow Jones Global Indexes® are registered trademarks or service marks of Dow Jones Trademark Holdings, LLC, used under license. Russell, Russell 1000®, Russell 2000®, Russell 3000® and Russell MidCap® names are registered trademarks of Frank Russell Company, used under license. FTSE® and the FTSE indices are trademarks and service marks of FTSE International Limited, used under license. MSCI and the MSCI index names are service marks of MSCI Inc. (“MSCI”) or its affiliates and have been licensed for use by Cboe. All other trademarks and service marks are the property of their respective owners.

Copyright

© 2022 Cboe Exchange, Inc. All Rights Reserved.

Related Posts